Claim your free €20 Bitcoin bonus now! Just verify your ID. Weekly payouts every Friday! Don't invest unless you're prepared to lose all the money you invest.

How digital money will include the unbanked

February 4, 2015

Basic financial services are more expensive and exclusive than they need to be. If we can strip digital finance down into a lightweight, near-free service, we can offer it to everybody, including those currently excluded from the sector.

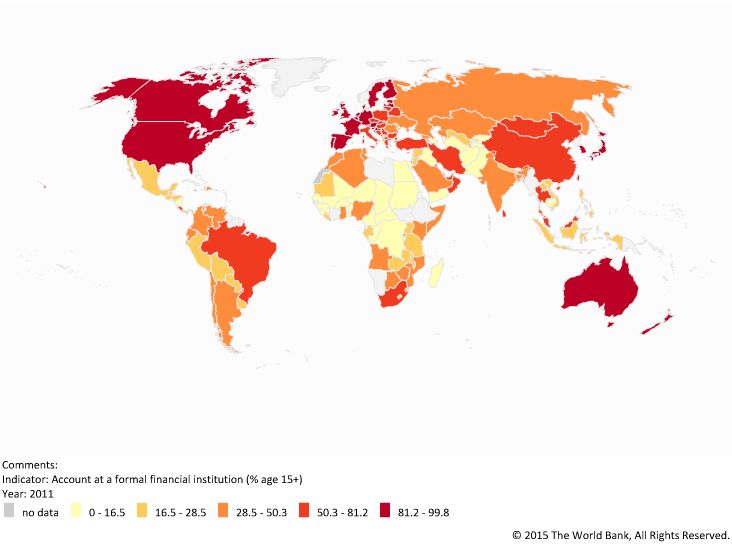

Approximately half of the adult world does not have a bank account. Billions rely on cash and informal credit arrangements to manage their finance, arrangements which tend to be slow, expensive, and unreliable. Given that we are finally making progress on the basic challenges in development, such as those in the Millennium Development Goals, it is not unreasonable to put some focus on second-order obstacles like connectivity, energy, and banking. Interestingly the Gates Foundation, which has long focused on public health, sanitation, and education, signaled this month it was shifting some of its focus to financial inclusion.

So how bad is it? Access to banking is minimal in large parts of sub-Saharan Africa, the Middle East, and Central Asia. Many middle-income countries also fare poorly, according to the World Bank four-fifths of Indonesians, two thirds of Indians, and one third of Chinese have no formal banking services.

The problem is not exclusive to the developing world, an astonishing 12% of Americans do not have bank accounts. While Europe and Australia fare relatively better, across the developed world there are millions classed as unbanked or underbanked. The reasons some residents of rich countries remain excluded from banking are complex, but are closely linked with poverty and other forms of exclusion. Citizen’s Advice Scotland found in its that among its unbanked clients, almost half had been denied a bank account because of poor credit history and a further one fifth because of current or historic debt with the bank.

Many of those were initially pushed out of the banking system because of bankruptcy proceedings. Thus the very people struggling to get back on their feet are the ones being locked out of our financial infrastructure. The same research found that one third of unbanked clients had been denied a bank account “due to lack of appropriate identity documents”.

In this part of the world most people excluded from banking end up using a family member’s bank account by proxy, so people are forced into informal banking arrangements by the very measures designed to ensure that the name on an account matches the person using it. This is part of wider problem of how restrictions designed to target wealthy criminals create a financial burden that falls largely on the poor, a topic which financial thinker .

“Thus the very people struggling to get back on their feet are the ones being locked out of our financial infrastructure.”

There is also a non-trivial number of people living in rich countries who are “unbanked by choice”, a result of mistrust, suspicion, alienation, concerns about unresolved debt, or a general sense of a bank account not being for them. The reason the banks themselves allow this to continue is that the cost of servicing these prospective customers would generally outweigh the economic benefit they may bring. In other words, it is very difficult to make money out of somebody living on the fringes of society.

A source at a UK high-street bank tells us that for a bank to profit from a customer it needs them to hold about £1,000 at any time in their current account. For anything below that, the marginal cost to the business, from running a network of branches and so on, outweighs the benefit of an additional customer.

“The reason the banks themselves allow this to continue is that the cost of servicing these prospective customers would generally outweigh the economic benefit they may bring.”

The impact of digital money and digital banking

A number of companies are racing to resolve this conundrum by building the first truly digital bank, a lightweight service without the overheads of traditional high-street banking. One of the more prominent contenders in the UK is , though others exist. If that goal is achievable, a digital bank will quite suddenly be in a position to target populations that are currently underbanked, providing them with near-free banking services while still turning a profit.

At our focus is on digital tokens rather than traditional monetary forms, but the question of unbanked populations goes to the core of what we do. Our goal is to take the efficiencies of Bitcoin, port them to a platform that is safe, simple, and secure, and push them out to the market at near-free prices. We do not believe in tiered pricing or access, every customer gets the same rates and support, regardless of the numbers involved when they want to and other digital currencies.

“…the question of unbanked populations goes to the core of what we do”

As a company we are betting on two broad trends in finance. The first is the unbundling of consumer finance products. In a world of bricks-and-mortar banks it makes sense to get your current account, mortgage, payment card, and insurance via the same relationship. In a digital world, it should be much easier to shop around for each of those services separately, and have them seamlessly interact with each other where necessary.

Our second expectation is that people will get used to interacting with a much richer variety of digital tokens. These might include air miles, loyalty card points, tokens for various corporate and community schemes, in-game currencies, tokens on social networks, kilowatt hours, carbon credits, contracts, and various other forms that don’t even have names yet. Such an ecosystem would allow rich and nuanced social and economic activity, and has interesting echoes in the past. To quote political economist Benjamin J Cohen, this would be a return to the “heterogeneous multiform mosaic that existed prior to the era of territorial money”.

Among these digital tokens is of course , the first big proposition in this latest round of monetary debate. One of the easiest ways to understand how Bitcoin behaves is to think of it as digital cash, albeit cash denominated in the currency of a distant, imagined country. While most discussion of Bitcoin focuses on the technical and socio-political aspects of the protocol (open and distributed security, a transparent but noisy ledger, a volatile market value, and a governance method modelled on open source software schemes), the very mundane functionality of a digital currency has massive implications for the underbanked. The creation of an account (or digital “wallet”) is effectively free and instant, largely unrestricted, and serves rich and poor with equal speed.

Indeed it is this detachment of the service from a bank-customer relationship, this unbundling, that may allow digital currencies to thrive among communities currently neglected by finance. As anthropologist Bill Maurer described:

“The un- and underbanked traditionally haven’t been served by traditional banking institutions. They’re the ones who are going to check-cashing outlets and pawn shops. They’re the ones where there really are pain points associated with checks and cash, for whom prepaid cards or prepaid wallets on a phone might actually be very attractive.”

The ability to store and transfer value is ultimately an informational good, so the sector likely faces a transformation comparable to what we’ve seen in music, publishing, and the visual arts. Some of those changes will be good (services get cheaper and faster) and some will be bad (services fall under oligarchic control and lose the human touch). Research by digital agency Heist indicates this transition has already commenced, with young adults having an increasingly “transactional” relationship with their bank rather than something more personal or advisory.

Making finance competitive is a hugely complex problem, the sector serves as a unique form of infrastructure which supplies us with money (created via fractional reserve lending) and the facilities needed to move that money around. The importance of appearance and legitimacy mean that much of the sector’s cost structure resembles that of a luxury goods company, with glass-and-steel skyscrapers, oak-panelled lobbies, and a general air of largesse which assures the client that everyone in the room knows what they’re doing.

You can’t run a bank like a budget airline when your customers still expect you to operate out of a city-centre building with Roman columns and reassuringly lush reception. Add to these peculiarities a few decades of overlapping regulation, uniquely powerful entrenched stakeholders, widespread misconceptions about how the sector works, and the shadow of both national politics and class politics, and it becomes clear that it will take more than a Napster-style disruption to shake up the sector.

“You can’t run a bank like a budget airline when your customers still expect you to operate out of a city-centre building with Roman columns and reassuringly lush reception.”

Nonetheless, banking is steadily evolving into a digital service, and in the process it should become easier to ensure that those who need it most have access. Nobody needs a credit check to start using a physical wallet, a digital wallet should be no different. If we want this infrastructure to be truly inclusive and competitive it should be built around an open platform with open standards. We want to see the Email of Money, not the Facebook of Money. And finally, we want this platform to undermine the imbalances between developed and developing worlds, rich and poor, not reinforce them.

What do you think? Tweet Lui @yablochko.

This article originally appeared on on 4 February 2015.

‘The Streets – Colourful Miraflores’ by Geraint Rowland available at under a Creative Commons Attribution 2.0. Full terms at http://creativecommons.org/licenses/by/2.0.

Don’t invest unless you’re prepared to lose all the money you invest. This is a high‑risk investment and you should not expect to be protected if something goes wrong. Take 2 minutes to learn more: .

Cryptoassets traded on CoinJar UK Limited are largely unregulated in the UK, and you are unable to access the Financial Service Compensation Scheme or the Financial Ombudsman Service. We use third party banking, safekeeping and payment providers, and the failure of any of these providers could also lead to a loss of your assets. We recommend you obtain financial advice before making a decision to use your credit card to purchase cryptoassets or to invest in cryptoassets. Capital Gains Tax may be payable on profits.

CoinJar’s digital currency exchange services are operated in Australia by CoinJar Australia Pty Ltd ACN 648 570 807, a registered digital currency exchange provider with AUSTRAC; and in the United Kingdom by CoinJar UK Limited (company number 8905988), registered by the Financial Conduct Authority as a Cryptoasset Exchange Provider and Custodian Wallet Provider in the United Kingdom under the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017, as amended (Firm Reference No. 928767).

EU residents: CoinJar Europe Limited (CRO 720832) is registered as a VASP and supervised by the Central Bank of Ireland (Registration number C496731) for Anti-Money Laundering and Countering the Financing of Terrorism purposes only.

On/Offchain

Your weekly dose of crypto news & opinion.

Join more than 150,000 subscribers to CoinJar's crypto newsletter.

Your information is handled in accordance with CoinJar’s .

More from CoinJar Blog

Your information is handled in accordance with CoinJar’s .

CoinJar Europe Limited (CRO 720832) is registered and supervised by the Central Bank of Ireland (Registration number C496731) for Anti-Money Laundering and Countering the Financing of Terrorism purposes only.

Apple Pay and Apple Watch are trademarks of Apple Inc. Google Pay is a trademark of Google LLC.

This site is protected by reCAPTCHA and the and apply.